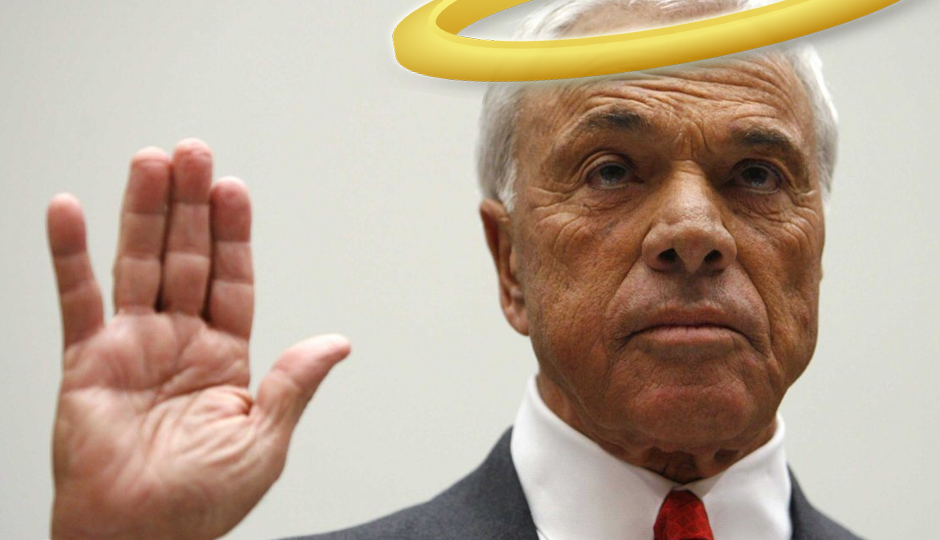

Moody’s hit for role in mortgage crash

Last Friday the Department of Justice (DOJ), along with Attorneys General in 21 states, resolved a federal investigation into Moody’s Analytics’ role in the financial crisis.

![]()

While mortgage lenders and investment banks certainly played a leading role in the mortgage meltdown, credit-rating agencies were a strong supporting role. The DOJ investigation looked into allegations that Moody’s was rating mortgage-backed securities and other financial products higher ratings than was merited, out of fear that rating realistically would lead financial institutions to take their business elsewhere.

Rating the same institutions that pay them is a huge conflict of interest, but Moody’s has long claimed their ratings are based on strict credit rating standards. However, the DOJ investigation concluded Moody’s was using an extremely lenient ratings standard.

The problem stems back to 2001

Problems were evident even in back in 2001, when Moody’s introduced an internal rating tool that utilize the company’s established rating standards. The company failed to announce changes in rating models and standards to the public, allowing them to mislead investors.

As it turns out though, several banks and lenders were well aware of Moody’s skewed rating system.

The Justice Department’s investigation uncovered internal communications from 2007 showing senior management were aware that mortgage-backed security ratings were not quite right. And by not quite right, I mean green-lighting seriously inaccurate ratings that contributed to investors believing securities were low-risk (which history has proven to be untrue).

Moody’s to pony up $864M

The DOJ announced the case settlement comes in around $864 million, with about half going to federal civil penalty and the rest divided up among the 21 states in involved in the investigation. While this is a relatively large chunk of money, others involved in the mortgage meltdown didn’t get off so easy.

For similar allegations, Standard & Poor (S&P) ended up shelling out a bit over a billion.

Moody’s apparently sees very little problem with their role in the financial crisis. In a press release the company stated, “Moody’s stands behind the integrity of its ratings, methodologies and processes, and the settlement contains no finding of any violation of law, nor any admission of liability.”

In spite of this, they company will adhere to compliance measures for five years, which they note is “final and is not conditioned on court approval.” While they can act like they’re just being good guys playing along with the DOJ, some lawmakers are calling for changes in how we deal with conflict of interests for credit-rating businesses.

Lawmakers call for change

Senator Al Franken suggests creating an independent agency that would assign rating jobs, effectively reducing the threat of lost business for inaccurate ratings.

Regardless of the steps taken to minimize problems in the future, the fact remains that many lax standards allowed companies to get away with some pretty shady dealings.

We need to not just look at how to prevent this, but also which practices we allow to remain in place. An independent agency overseeing ratings is certainly a step in the right direction, but businesses must also create and maintain an internal culture of integrity if we want to avoid another meltdown.

#MoodysFine