Square mobile payments gets 1233% better

With the push on for more and more businesses to accept mobile payments, the offer of additional features from the payment providers can make a big difference in which platform a business chooses. Popular payment tool, Square, has introduced a new analytics tool designed to give sellers new data to increase sales.

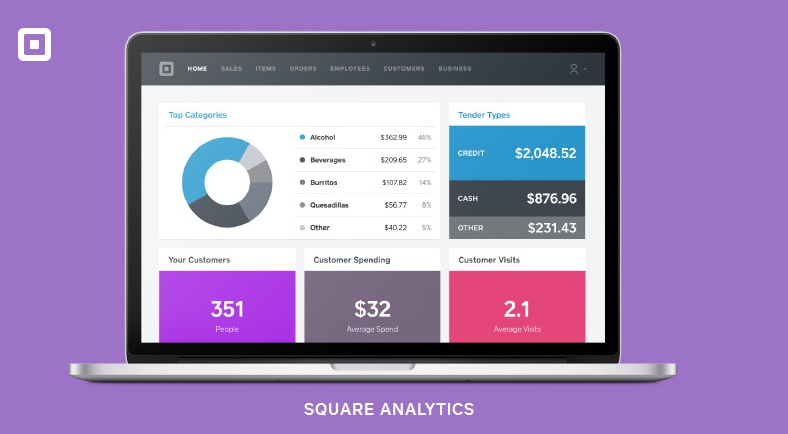

The new app, Square Analytics, is designed to “level the playing field” for small companies because it delivers easy access to stats and analyses that were previously reserved for big companies, with budgets affording them access to these tools.

![]()

Square Analytics aggregates information from their point-of-sales (POS) tool, Square Register. This includes: invoices, customer spending data, tender types, inventory, and appointments. The Square Analytics tool is also optimized for mobile monitoring.

This means you can see how your business is doing in total sale by the week, month, or compare figures, on-the-go or in your office. It will also deliver a daily summary of your account to your inbox, making it easy to see the day’s total’s without leaving your inbox.

Adding even more insight into your business

If you connect your Square account to leading accounting services like QuickBooks, Xero, or even create your own with Square Connect API; you can gain an even deeper insight by by seeing your sales alongside your your budget. You can also sync with Stitch Labs for an analysis of your inventory.

Square Analytics breaks sales down to the item, so you can see what is popular, and what is not. You can also see if you need to stay open longer, or if you need to restock. Allowing you to understand your business a little bit better. It is not just about numbers, however, you can also understand your customers in a whole new way. Identify new versus returning customers, and find out how much your average customer is spending. Discover which products or services are drawing people in, and which need to go.

While these additional features are certainly helpful for established businesses who have a little history with Square, I am not sure how much this will benefit new companies, as there will be no data to aggregate. Also, some companies may not benefit very much from this feature simply because the majority of their payments are not at a POS terminal.

However, if your business has been accepting Square payments for a month or more, this could give you valuable insight into your strengths and weaknesses, that you would otherwise pay extra for elsewhere. I do think if Square is truly interested in “leveling the playing field” they should consider reducing their fee by as little as 0.25 percent, this would tip the competition a bit further in their favor, in my opinion.

If you frequently use Square, check out the recently launched IFTTT Square recipes to automate everyday tasks. You can automate everything from adding a line to spreadsheets and creating new settlements in Evernote. Another great way to save time.