PayPal.me is pretty slick

In 2014, PayPal moved 26 different currencies totaling $228 billion throughout 190 nations. Since its inception in 1998, it has practically dominated the online payment industry as a subsidiary of Ebay until earlier this year when it became an independent company. Now that it operates separate from Ebay, it’s moving into its own identity.

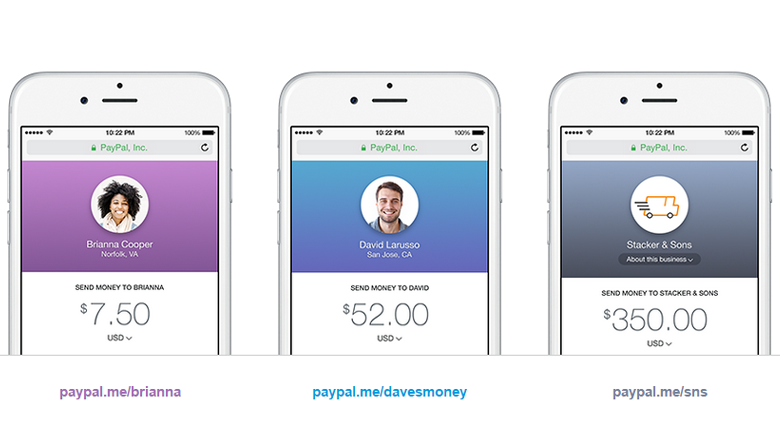

One of PayPal’s newest offerings is a personalized link that you can send to friends, family, and coworkers, to pay you through PayPal. It’s called PayPal.me and it works through text, email, IM, social media or blog post.

![]()

You can use your own name or the name of your business to create the link and there is a picture that is connected to the link which means that friends and customers are assured it is your link. Preferred links are on a first-come, first-serve basis. Reserved trademarks are forbidden, as are offensive or derogatory names. If you violate this, your account may be suspended.

The trick? Both parties need to have PayPal accounts

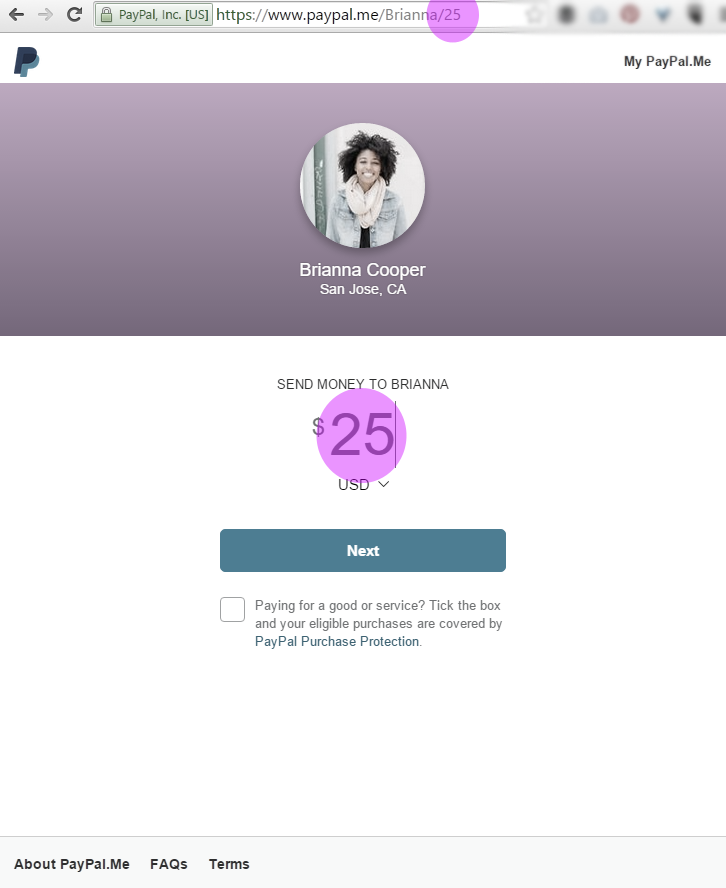

You do need a PayPal account to set up the PayPal.me link. Your payee will need an account also. You send them the link, with or without an amount (with the amount shown below). They tap on the link, confirm the amount, and send money through their own PayPal account.

When sending money through the same country, it’s free for you to receive money. There are fees associated with a PayPal Business account or when using the PayPal Purchase Selection “goods and services.” When operating between countries, you will need to look at the fee schedule provided by PayPal.

Security is the same as with PayPal

PayPal.Me uses the same security as PayPal, which means that your transaction is protected. The only information shared through the link is your name, the profile photo, and your location (city, state, country). This lets your customers and friends know they are paying the right person.

The money instantly shows up in your account. Instead of chasing co-workers or clients for money, PayPal.Me makes it easy to get what you’re owed.

#PayPalMe

David

July 19, 2016 at 1:52 am

“Since its inception in 1998, [PayPal] has practically dominated the online payment industry as a subsidiary of Ebay until earlier this year when it became an independent company.” No, PayPal did not start out at as a part of eBay. eBay bought it in 2002, after it had been in existence for years.