The national average credit score is at an all-time high of 716, up 26 points since October 2012.

Typically we see a slight uptick each year, but this marks the first year since the Great Recession that the average score did not improve. Let’s take a look at the trends and how your location may impact your credit score and lending opportunities.

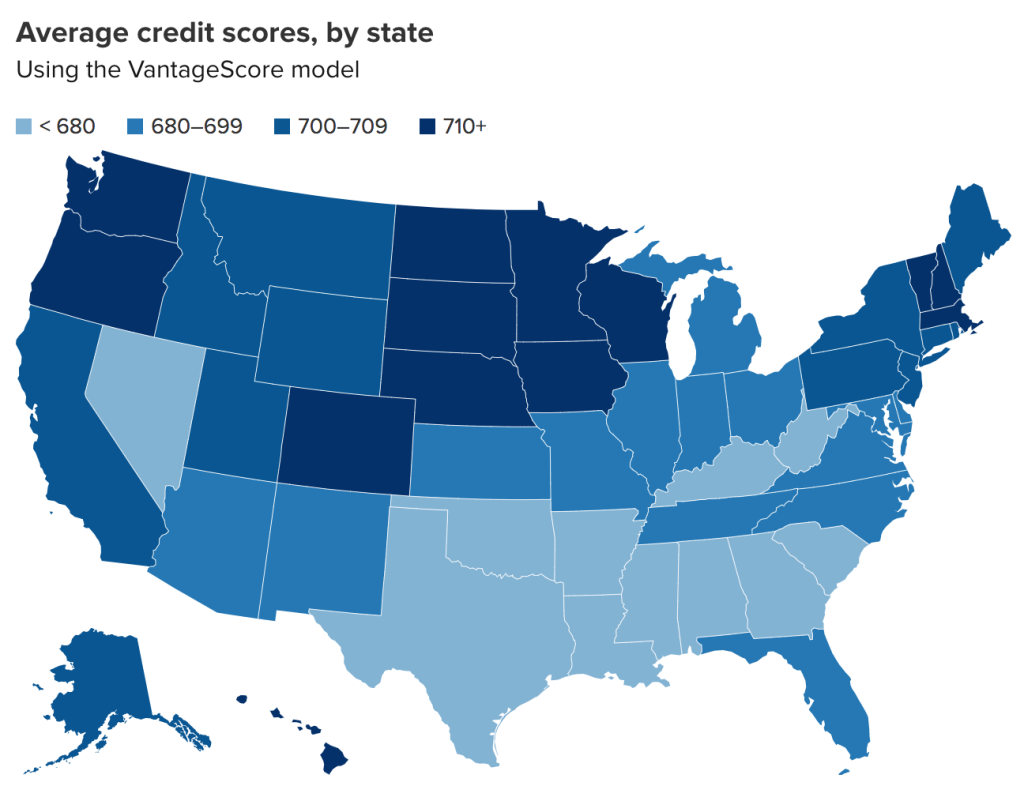

According to WalletHub, Minnesota ranks highest with an average credit score of 724, which sits above the national average, and even that of wealthier states like California and New Jersey. Part of this may be thanks to a higher-than-average employment rate and a lower-than-average poverty rate. New Hampshire, Vermont, and Massachusetts follow closely behind.

Mississippi ranks at the bottom of the spectrum with an average score of 662. Neighboring states Louisiana, Alabama, and Arkansas keep them company with low scores, despite offering a fairly low cost of living.

On average, southern states have shown the lowest national credit scores while the midwest, northeast, and west coast show higher than average scores.

It’s common knowledge that lenders advise borrowers to keep rotating credit utilization under 30% for the best odds of approval and lower interest rates, but as of April 2022, we’ve seen a national average of 31%, up from 29.6% in 2021. We’ve seen credit card balances soar over 15% as well as more frequent reporting of missed payments.

Before entering a lending agreement, you may find it worthwhile to consider inflation, your local job market, and the cost of living in your current location. The Covid-19 pandemic has hit some areas of the US with terrible misfortune, especially since the roll-back of government stimulus and assistance programs. Some Americans may find it difficult to find their bearings after falling into pandemic-related debt, so it’s important to know the credit trends in your area before entering a lending agreement.

Despite the unchanged national average, FICO vice president, Ethan Dornhelm, has not expressed much concern.

“We are leveling off back to pre-pandemic norms which is, in and of itself, not a red flag,” Dornhelm said, despite “this slight deterioration of debt levels. What we’re keeping an eye on is if there’s continued deterioration.”

Do any of these state-based averages surprise you? We’d love to know your thoughts.