SalesMaple is out to impress

With salespeople needing to sift through so many tools to help them accelerate, predict, and enable their sales opportunities, it’s a wonder they have time to do anything else.

While there are multiple tools available for salespeople to optimize their opportunities, selecting the right one can be frustrating and time consuming. SalesMaple aims to remedy this by simplifying the sales prediction platform.

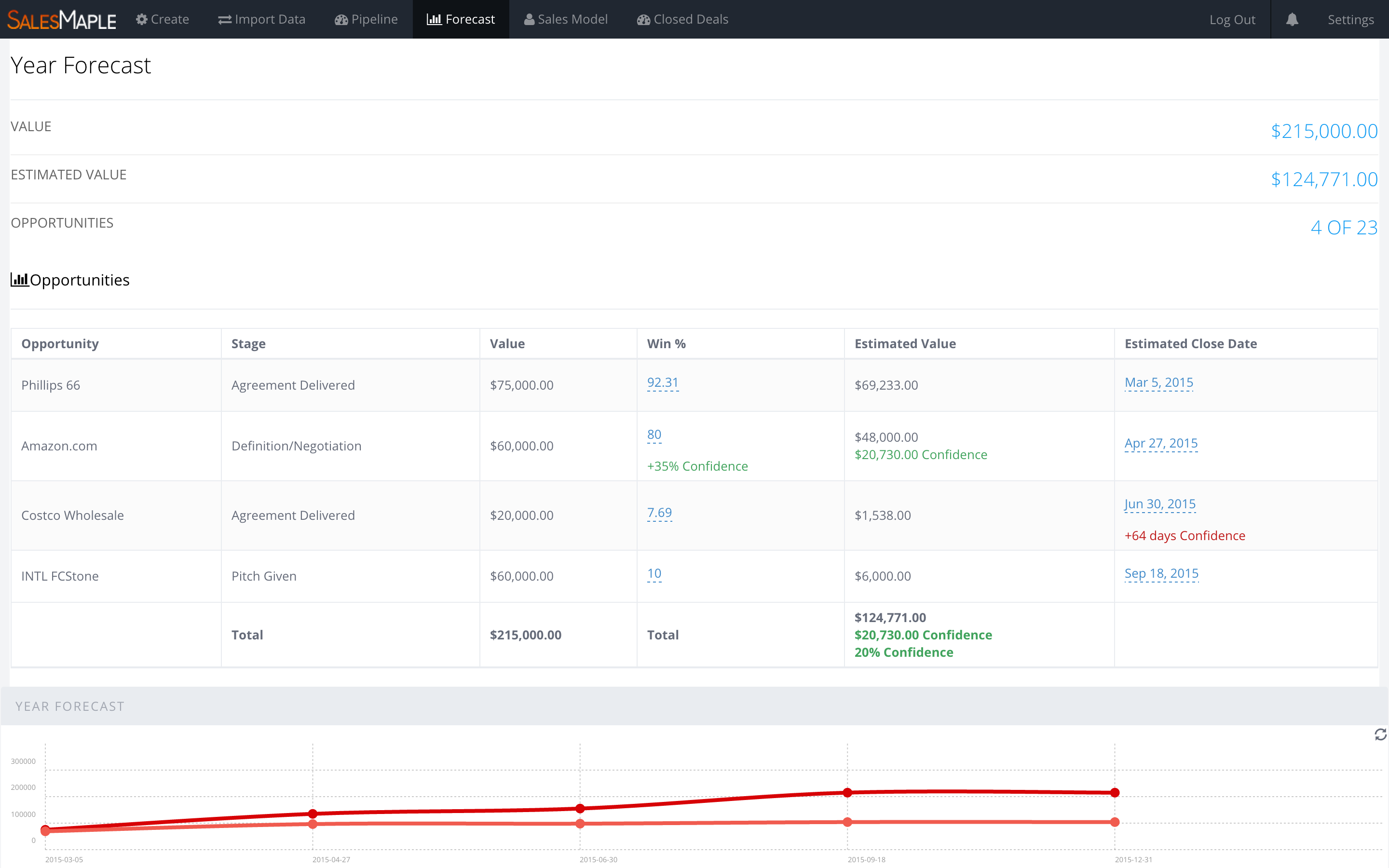

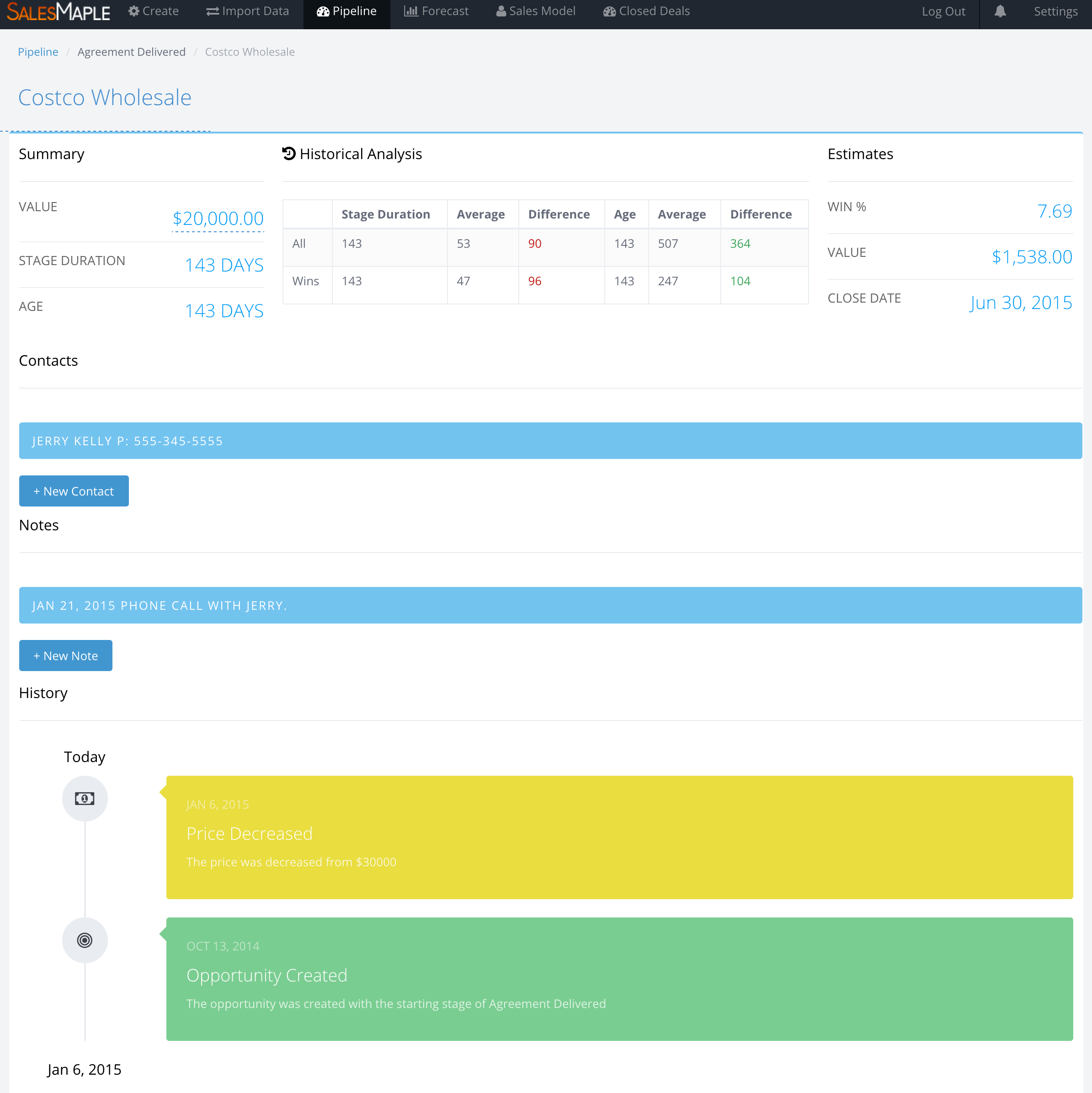

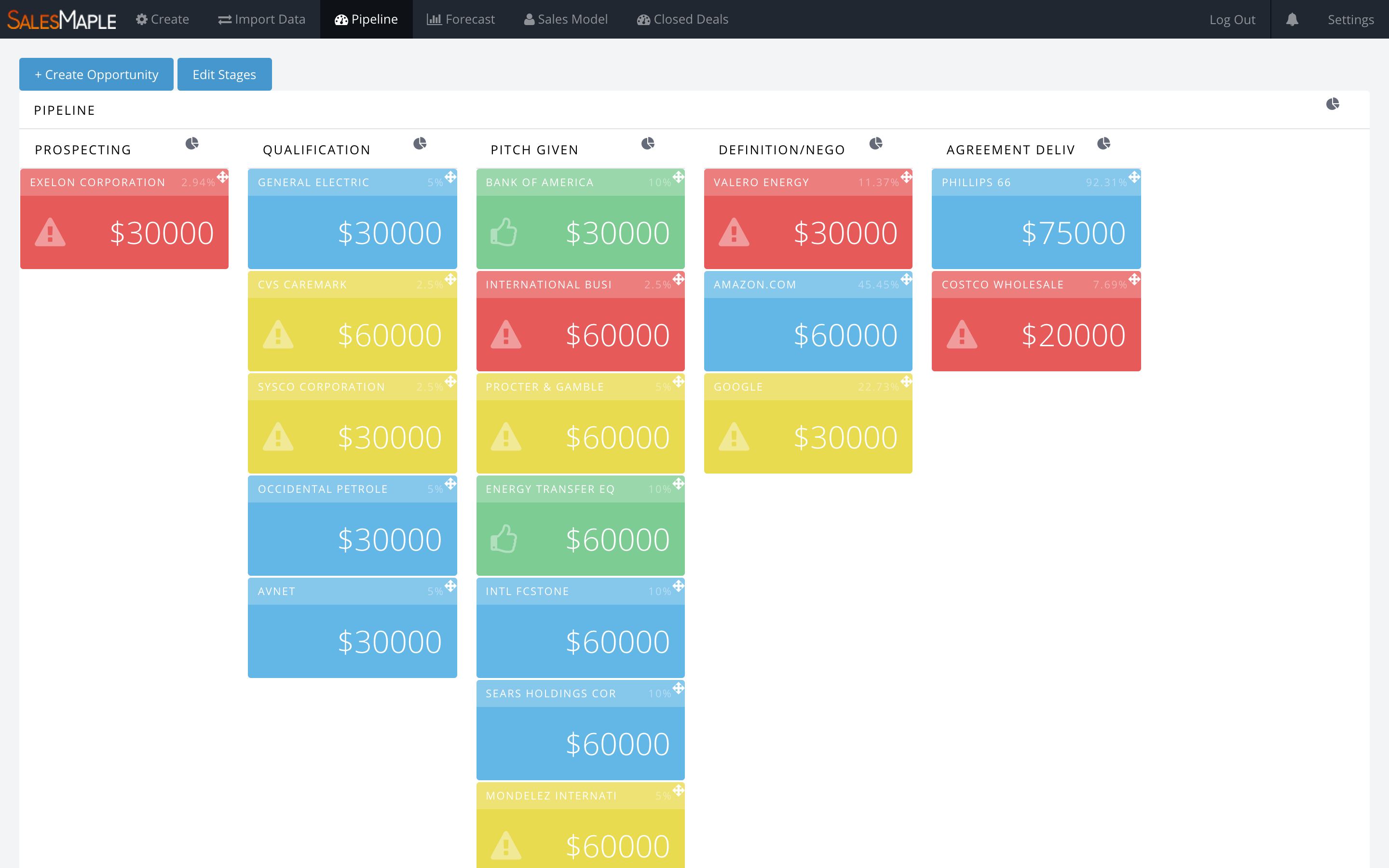

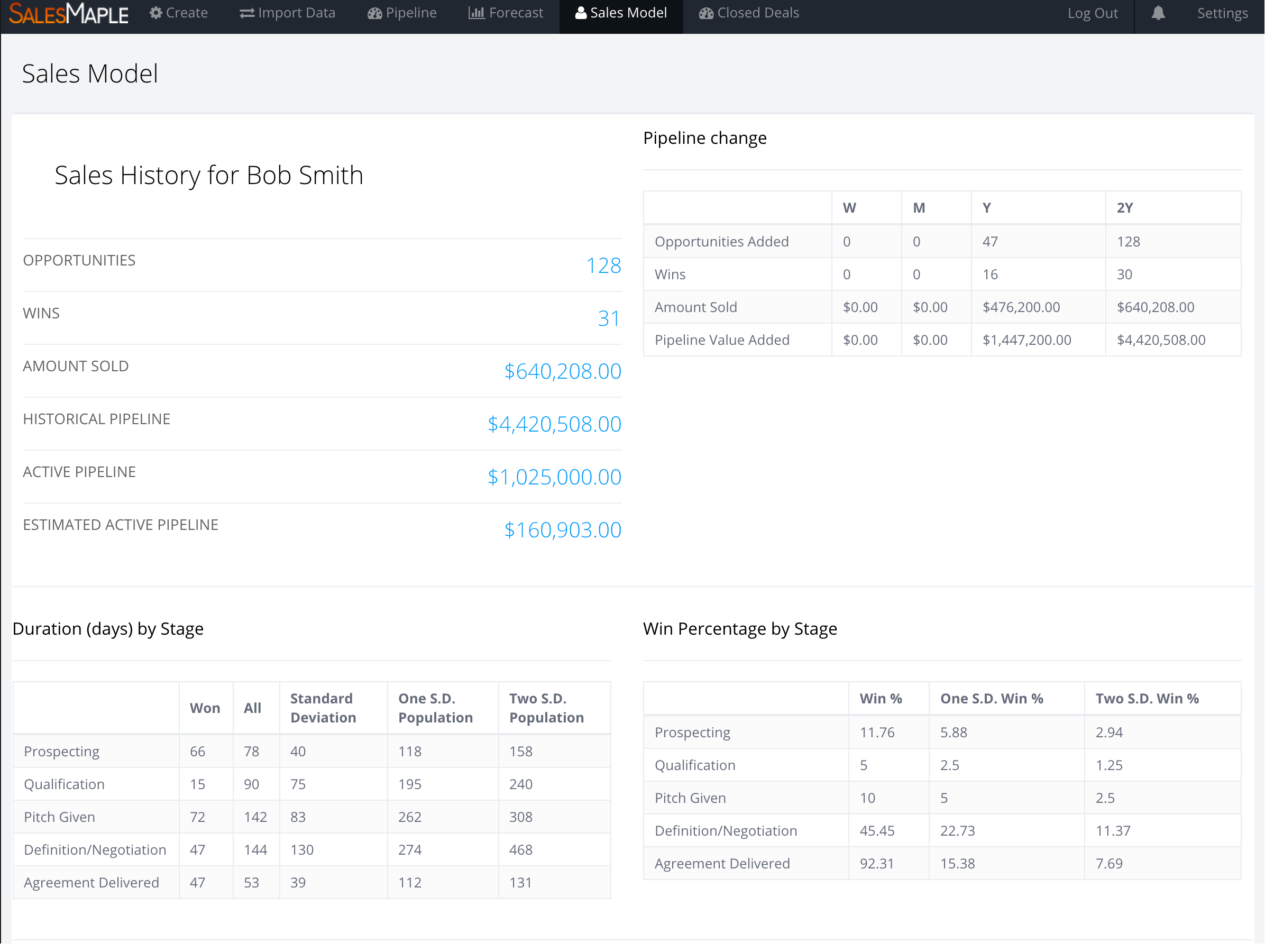

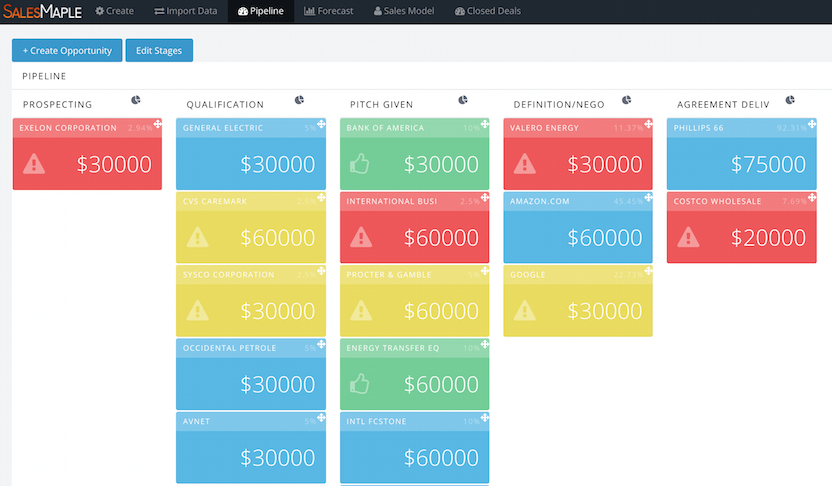

SalesMaple is a sales reporting, dynamic analysis, and dynamic prediction platform that continuously builds prediction models for individual sales people in order to provide intelligent sales pipeline management and forecasting. It helps small-to-medium businesses (SMB) manage their pipeline for effectively.

![]()

SMB pipeline management is especially important since selling styles among salespersons can vary greatly and cause company wide statistics to vary; rather than trying to manage each person’s style and subsequent changes, SalesMaple keeps track of it for you.

One hell of a prediction modeling engine

The SalesMaple platform has a prediction modeling engine that identifies which stage and population each sales opportunity is in, then applies analysis statistics to active opportunities. This engine is then rebuilt every time the analysis data is updated, allowing it to be reapplied to new opportunities. It also rebuilds every time the opportunity’s data (stage, duration, value, etc.) changes. It also integrates with with Salesforce; syncing all SalesMaple and Salesforce data back and forth seamlessly.

The platform is flexible to accommodate each salesperson’s individual style because each person’s style can directly impact the duration and likelihood of a win from each stage, even when the same processes are followed.

Simple aggregation perfect for any leader

If you’re a manager, sales opportunities and forecasts will be aggregated for you. This aggregation is continually updated as sales reporting, analysis, and modeling are updated. The manager can see company wide statistics, but the predictions for each opportunity are always based on the individual salesperson’s model. The sales manager can also split a team in half, in order to try out a new sales strategy (A/B sales testing).

If you’re looking to try a new sales strategy, implement subtle changes, or just getting started, SalesMaple may be a good option for your SMB.

#SalesMaple