The yearning to own your own home has been and still is something people really want. According to the most recent Profile of Home Buyers and Sellers report by The National Association of Realtors® (NAR), data shows first-time and repeat buyers are still financing homes. The survey, which “allows industry professionals to gain insight into detailed buying and selling behavior” since 1989, surveyed buyers and sellers who purchased between July 2019 to June 2020.

How much do home buyers finance?

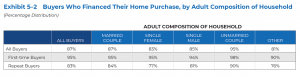

The NAR report shows 87% of all home buyers financed their home in 2020. This is up 1% from last year. First-time buyers are more likely to finance their homes more than repeat buyers with 95% and 83%, respectively.

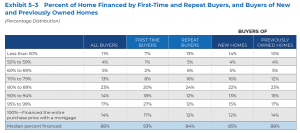

Also, 14% of all home buyers financed 100% of the entire cost of their home using a mortgage. First-time buyers’ median percent of finance was 93%, and it was 84% for repeat buyers. Overall, the median percent of finance for all buyers was 88%.

Does everyone put 20% down?

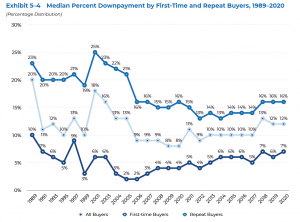

According to the NAR report, the median down payment for all home buyers was 12%. Among first-time buyers, it was 7%, it was 16% for repeat buyers. For the most part, down payments have either gone down or stayed about the same since 2005.

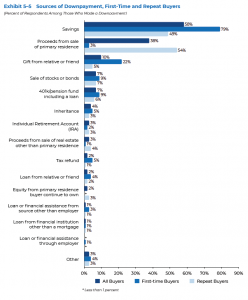

Over half (58%) of recent home buyers said they used their savings for financing their home purchase. This is a 2% decrease from last year but is still higher than the historical norm of 55% since 2000. Also, 38% of homeowners said they used proceeds from the sale of a primary residence to finance their new home, the same as last year.

For repeat buyers, 54% cited using proceeds from their previous sale to finance their new home. In 2014, it was 47%, and 25% in 2012. The high increase could be due to the increase in property values over time. On the other hand, 79% of first-time buyers used savings, and 22% used a gift from family or a friend to finance their home.

Home Buying Obstacles

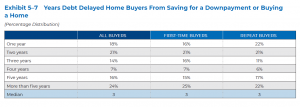

For 24% of home buyers, some sort of debt was cited as a reason for having to delay purchasing a home. Home buyers waited a median of 3 years to save for a down payment and lower debt before buying a home.

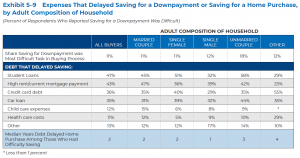

For home buyers, 11% said saving for a down payment was the most difficult step in the home buying process, down 2% from last year. Expenses that made it difficult to save were student loans (47%), high rent or current mortgage payment (43%), and credit card debt (36%). To make a purchase, some home buyers made financial sacrifices like reducing spending on luxury or non-essential items (23%) and cutting entertainment spending (15%).

Is purchasing a home a good financial investment?

According to the NAR report, 83% of home buyers did view buying a home as a good investment, and 42% said it was even better than owning stock. Also, 85% of first-time buyers see it as a good financial decision compared to 82% of repeat buyers. For unmarried couples, it was 86%.

Overall, the NAR report shows first-time and repeat buyers are still financing to purchase a home. Repeat buyers tend to put more money down on a house using money from a previous home sale. First-time buyers tend to put less money down and use their savings. And, debt is without a doubt, the reason why most buyers delay purchasing a home.