PropTech has flooded the real estate space over the last few years, claiming to provide a superior way to transact. Moreover, many of these firms have an unseemly arrogance and demean traditional real estate professionals while often misleading consumers.

I suggest reading the Terms of Service (TOS) for each PropTech firm. You may discover that most consumer-facing home page representations are completely offset, and the TOS limits consumers’ dispute remedies.

If a firm claims it will “list/sell your home for $3,500” and offsets these representations via liability or indemnification obligations in the TOS, the organization, in my view, cannot be trusted.

Language often includes:

IN NO EVENT WILL “Dumpster fire Real Estate Inc,” ITS OFFICERS, SHAREHOLDERS, EMPLOYEES, AGENTS, DIRECTORS, SUBSIDIARIES, AFFILIATES, SUCCESSORS, ASSIGNS, SERVICE PROVIDERS, OR LICENSORS BE LIABLE FOR (1) ANY INDIRECT, SPECIAL, INCIDENTAL, PUNITIVE, EXEMPLARY, OR CONSEQUENTIAL DAMAGES; (2) ANY LOSS OF USE, DATA, BUSINESS, OR PROFITS (WHETHER DIRECT OR INDIRECT), IN ALL CASES ARISING OUT OF THE USE OF OR INABILITY TO USE THE PLATFORM, SERVICES, OR CONTENT, REGARDLESS OF LEGAL THEORY, WITHOUT REGARD TO WHETHER “Dumpster fire Real Estate Inc,” HAS BEEN WARNED OF THE POSSIBILITY OF THOSE DAMAGES, AND EVEN IF A REMEDY FAILS OF ITS ESSENTIAL PURPOSE. IN NO EVENT WILL “Dumpster fire Real Estate Inc,” TOTAL LIABILITY FOR ANY CLAIMS ARISING OUT OF OR IN CONNECTION WITH THESE T&CS OR FROM THE USE OF OR INABILITY TO USE THE PLATFORM, SERVICES, OR CONTENT EXCEED THE AMOUNTS USER HAS PAID TO “Dumpster fire Real Estate Inc,” FOR USE OF THE PLATFORM, SERVICES, OR CONTENT IN THE THREE (3) MONTH PERIOD IMMEDIATELY PRECEDING THE EVENTS GIVING RISE TO THE APPLICABLE CLAIM. THIS SECTION APPLIES TO THE FULLEST EXTENT PERMITTED BY LAW.

Also, if a Company displays numerous five-star reviews yet denies the ability to leave a review on their website, this may suggest online review manipulation.

Let us explore the key former and current PropTech companies:

In what follows, stock prices depicted are from the prior 12-months as of publication.

1. PurpleBricks

Crickey, did you retreat to Australia? Did your flat fee ~$3,500 listing service fail? Did you tell Homie? Regardless, nice knowing you.

2. Zillow (NASDAQ -55.05%)

The iBuying program, meant to simplify the selling process, failed spectacularly. Zillow’s reputation with Agents is diminished. Lawsuits are prevalent. Premier Agent/Lender reviews are suspiciously high.

Moreover, Zillow’s Rental Manager Program displays a small fraction of available rentals as it appears that Zillow only shows rental properties listed by owners or property managers who pay Zillow a weekly fee. The fee is excessive, and in my view, disproportionally impacts lower-priced homes.

Compounding this act, Zillow fails to disclose this limited display deficiency to consumers and steers them to apartment complex ads.

It might be time to revisit NAR CODE 12.8.

Moreover, Zillow’s 8k disclosure discusses legal proceedings and in relevant part: “Certain of the plaintiffs also allege, among other things, violations of Section 14(a) of the Securities Exchange Act of 1934 and waste of corporate assets. On February 5, 2018, the United States District Court for the Western District of Washington consolidated the two federal shareholder derivative lawsuits pending in that court. On February 16, 2018, the Superior Court of the State of Washington, King County, consolidated the two shareholder derivative lawsuits pending in that court. All four of the shareholder derivative lawsuits were stayed until our motion to dismiss the second consolidated amended complaint in the securities class action lawsuit discussed above was denied in April 2019. On July 8, 2019, the plaintiffs in the consolidated federal derivative lawsuit filed a consolidated shareholder derivative complaint, which we moved to dismiss on August 22, 2019. On February 28, 2020, our motion to dismiss the consolidated federal shareholder derivative complaint was denied. On May 18, 2020, we filed an answer in the consolidated federal derivative lawsuit. On August 24, 2020, we filed an answer in the consolidated state derivative matter. We do not believe that there is a reasonable possibility that a material loss will be incurred related to this lawsuit.”

In my view, Zillow is not a nominal defendant, and the “derivative” claim fails to disclose the gravity of this case.

The lawsuit alleges that Zillow operated an unlawful, RESPA violating co-marketing scheme.

RESPA is a license revoking act.

A regulatory storm will be imposed. Good riddance Zillow, it has NOT been a pleasure.

3. Redfin.com (NASDAQ -42.91% YTD)

In my view, Redfin is the most honest PropTech firm in the real estate industry.

Redfin’s inability to consistently profit despite being founded in 2004 may have brought humility.

4. OpenDoor (NASDAQ -37.51% YTD)

Opendoor disclosed: “On December 23, 2020, the FTC notified us that they intend to recommend that the agency pursue an enforcement action against us and certain of our officers, if we are unable to reach a negotiated settlement acceptable to all parties. The FTC has indicated that they believe certain of our advertising claims relating to the amount of our offers, the repair costs charged to home sellers, and the amount of net proceeds a seller may receive from selling to us versus selling in the traditional manner were inaccurate and/or inadequately substantiated. We are engaged in settlement negotiations with the FTC.”

Further: “We have identified material weaknesses in our internal control over financial reporting and may identify additional material weaknesses in the future or fail to maintain an effective system of internal control over financial reporting, which may result in material misstatements of our consolidated financial statements or cause us to fail to meet our periodic reporting obligations.”

Opendoor now reveals the following on their pricing page: “* Beginning on September 30, 2020, for new offers, Opendoor’s service charge will be no more than 5%. Service charge is subject to change, and has historically been as high as 14%.”

If OpenDoor cannot consistently achieve profitability in an appreciating market when fees have “historically been as high as 14%,” how is capping fees at 5% viable going forward?

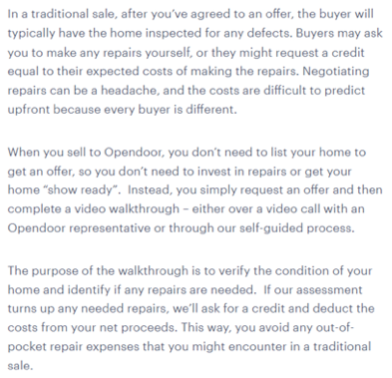

Moreover, help me to understand this claim… Opendoor’s first paragraph appears to frown against transacting via traditional methods as “they might request a credit equal to their expected costs of making the repairs.” The third paragraph admits Opendoor will ask for a credit and deduct it from the offer price.

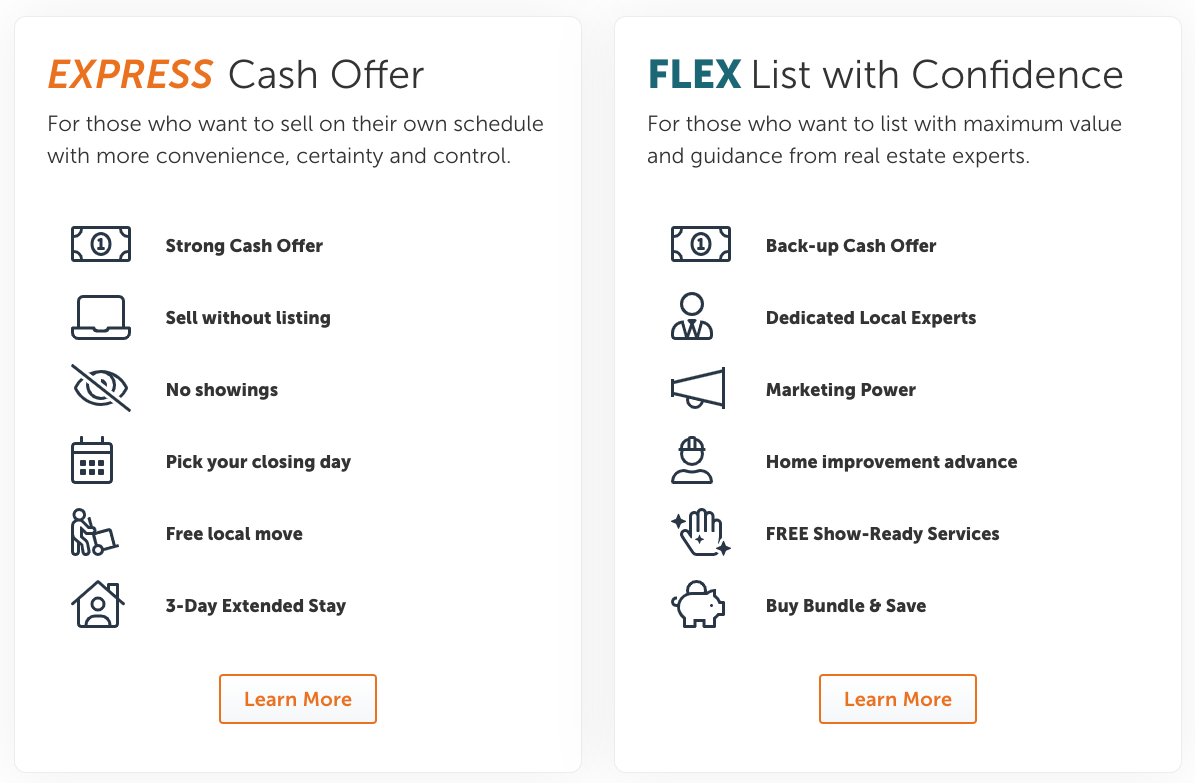

5. Offerpad (NYSE -37.69% YTD)

It appears that Offerpad has adjusted its services to provide iBuying and Agent aided transactions. Offerpad matched OpenDoor’s 5% cap and added a 6% listing fee if a Consumer wants to “list with maximum value and guidance from real estate experts.”

PropTech’s prior inferences are that agents are unnecessary and archaic. Furthermore, PropTech companies continue to assert that the 6% commission fee directly results from NAR’s price-fixing “cartel,” they claim.

The average MLS listing commission in 2021 was 4.94%, below Offerpad’s non-agent fee.

Did Offerpad join the NAR cartel and engage in price-fixing, or did they discover that market forces, NOT supra-competitive fees, determine 5-6% fees?

6. REX Homes

Who? I heard that REX Homes entered into the press release business.

Now, let’s move on to mortgage PropTech firms:

7. Better.com

Better’s website states: “When you work with Better Real Estate, you have a partner at every step.”

Is this claim still valid after CEO Vishal Garg laid off 900 employees, about 9% of the company’s workforce, in a three-minute Zoom call?

Question: If Better.com can fire you via Zoom, can an applicant gain employment via Zoom? Asking for a friend.

8. Rocket Homes

Good luck with the CFPB investigation.

Next up, property management firms

9. Home 365

Home365 claims they are “The Best Property Management Company.” They state, “Traditional property managers are offering little to negative value with owners’ and managers’ interests completely misaligned. Their old school methods lead landlords to lack predictable ROIs and trust issues. Landlords are often required to stay involved in every aspect of management making the entire experience annoying and costly. In fact, landlords compromise their investment by letting the “old world” manage their assets. We believe that your rental property is your money, your future, and your retirement. You deserve better and guaranteed returns.”

Your TOS is garbage, Home 365. They appear to list a meager 19 properties in Las Vegas. Furthermore, it seems that Home365 fails to display rentals on the MLS, which is the greatest marketing tool in real estate. Even us illiterate “old school” Realtors know this.

My firm is “old school” by your definition, and if we were to compare; Home365 is a swap meet, and LRA is Nordstrom.

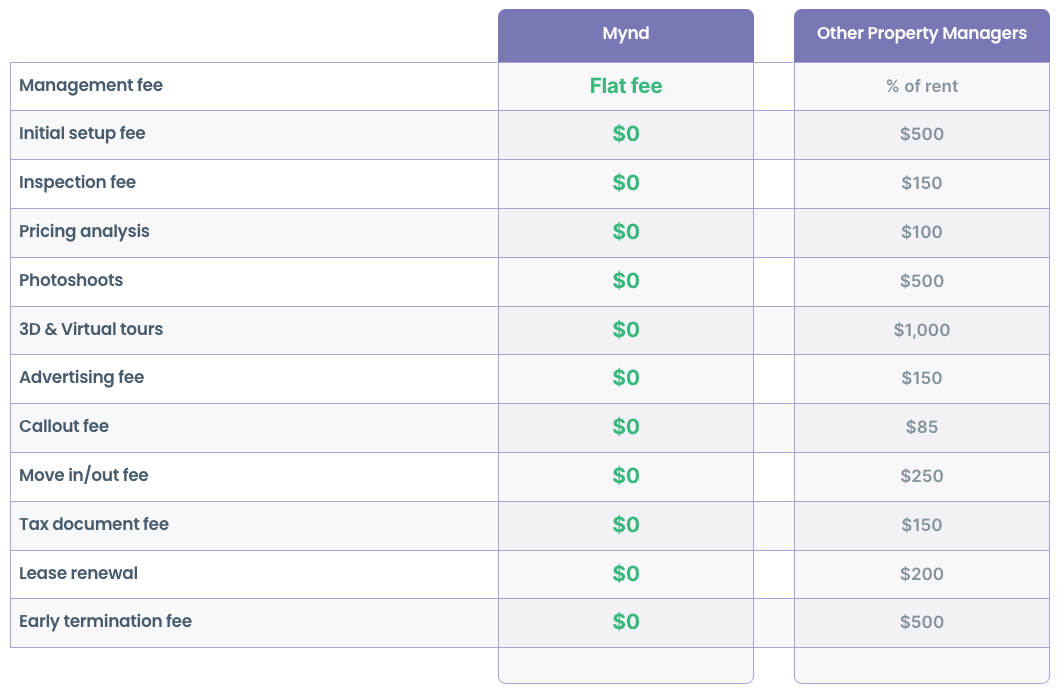

10. MYND

In my opinion, MYND may be the preeminent propagandist (now that REX is almost silent.) This is an amazing achievement. MYND displayed the following comparison to using “other property managers.”

These grossly exaggerated “other property manager” fees failed to include a widely imposed “document delivery by carrier pigeon fee,” which averages $12,000 per document.

There is also an AOL dial-up internet reimbursement fee.

Furthermore, MYND’s Oakland BBB page displays 107 Customer reviews averaging 2.9 of 5 stars and 127 complaints over three years.

Furthermore, MYND’s Oakland BBB page displays 107 Customer reviews averaging 2.9 of 5 stars and 127 complaints over three years.

When reviewing reviews, how did MYND achieve four amazingly generic five-star reviews on 11/8/2021? Also, why is there a lack of reviews since 12/10/2021?

Lastly, agent referral services

The majority of these firms are garbage.

These companies often claim they will find consumers the “best real estate agents” and “show local agents-it is free!” and Dave Ramsey’s referral company that asserts that “Your Values Are Their Values Too. You’re not getting suckered into a deal you don’t want.”

11. Ramsey Solutions

Ramsey’s ASSumption that other agents sucker clients into a deal they don’t want must be proven by peer-reviewed studies or deleted. Ramsey may sucker consumers, Realtors do not.

Moreover, participating in or being enriched via a real estate transaction often requires a license in each state. Is Ramsey licensed?

These assertions are amusingly misleading.

Further, let’s look at how are RamseyTrusted ELP agents are selected to be in the program:

- “Our agents go through a rigorous vetting process. After applying, potential pros go through a multi-step interview process. First, we make sure they meet these minimum qualifications:

- They’re in the top 10% of their market or close at least 35 homes per year.

- They have been in the industry for more than four years.

- They work with both buyers and sellers in all types of markets.

- They’re full-time, full-service—in other words, this isn’t some side gig.

- Next, we verify that applicants share Ramsey values—meaning they are on a mission to serve you, have the heart of a teacher, and agree to work with you according to our financial principles called the 7 Baby Steps. Keep in mind that only about 3% of new agents who applied to the program last year ended up making it in, so this isn’t a cakewalk.

- To stay in the program, agents must ace our Ramsey Pro Training Course and receive ongoing one-on-one and group coaching from our dedicated team. In addition, agents are scored by their coaches three times per year according to how well they served you. That way, there is a system of checks and balances in place to ensure that only quality agents get to stay in the program. “

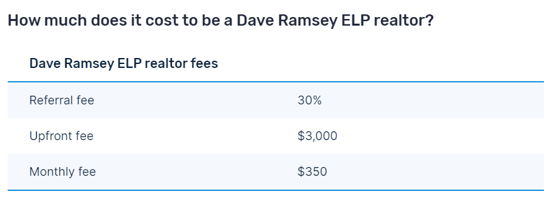

Does Ramsey also evaluate whether an agent can afford to pay a ~30% kickback fee?

If we review Ramsey Solutions, the agent information section states:

And…

Correct me if I am wrong: Representations of “free” apply specifically to the consumer, however an agent must allegedly pay excessive fees to become an “Endorsed Local Provider (ELP) real estate agent?”

This fee structure appears to exceed Zillow’s flex program.

Moreover, the “no warranty” claim that “Ramsey Solutions hereby expressly disclaims any and all warranties, including without limitation: any warranties as to the availability, accuracy, or content of information, products, or services; any warranties of merchantability or fitness for a particular purpose,” is perplexing.

Why does Ramsey exist?

I am a top Agent and would never consider third-rate referral services.

It may be appropriate to revise your Consumer representations to “When buying or selling a house; you want a real estate agent (that agreed to pay Ramsey a kickback) to negotiate the best deal and treats you as their most important client. That’s what you get when you choose one of our Endorsed Local Provider (ELP) real estate agents.”

Moreover, “Is Hiring an Agent Worth the Cost? Okay, now let’s answer the question you’ve been waiting for: Are real estate agents worth the cost? Well, as we covered earlier, sellers cover the commission for both agents. So, buyers have nothing to lose! But how about you sellers out there? If you’re considering not using an agent or going the “For Sale by Owner” (FSBO) route, first take a look at the stats. The latest data shows the typical FSBO home sold for $217,000 compared to $242,300 when sold by an agent. That’s a $25,300 difference!”

The $25,300 difference equals ~+10% when Realtor fees currently average 4.94%. Thank you for confirming that the benefit of listing with an Agent exceeds any detriment and results in superior net proceeds.

Stick to podcasts.

In summary:

I am aware that most of these websites attempt to bind visitors to contractual obligations merely by visiting their sites, and my analysis and commentary could allegedly violate these hidden TOS.

It is reasonable to infer that this article will compel a legal review by Ivy League legal teams to assess the merits of bringing a breach of contract claim against me.

Save the fancy letterhead and billables. If a claim is filed, I will not file a motion to dismiss, we can go straight to discovery, and I know precisely which executives and documents to subpoena and depose. Retaliating would be perilous. I have direct connections to Director level government officials, 17-class action firms seeking opportunities, and I spectacularly overreact.

PropTech has denigrated Realtors for years, which now ends.

How about being honest in 2022?

Your friend,

Anthony